Cross-Border Payments Roundup - October 2022

Welcome

Welcome to the second Cross-Border Payments Round-Up, a biannual newsletter sharing updates on the progress of the global roadmap for enhancing cross-border payments.

The Financial Stability Board's (FSB) 'Enhancing Cross-Border Payments Roadmap' aims to deliver faster, cheaper, more transparent and more inclusive cross-border payment services for all. Maintaining the safety and security of payment systems and platforms is paramount. Significant momentum has been achieved by the FSB and its partners as they pursue improvements in cross-border payments. In this issue, we highlight some of the key activities and output, as well as Australia’s response.

We also take a look at upcoming roadmap activities.

The FSB’s three priorities for the next phase of work to Enhance Cross-Border Payments

The FSB has published its 'Priorities for the next phase of work' for taking the Roadmap forward. The three themes they have identified and are focusing on for the next phase are:

- Payment system interoperability and extension;

- Local, legal and supervisory frameworks; and

- Cross-border data exchange and message standards.

Source: CPMI

Source: CPMI  Source: FSB

Source: FSB

Cross-Border Payments Advisory Council

AusPayNet's Cross Border Payments Advisory Council (CBPAC) continues to support and coordinate industry activities, including involvement in consultations and delivering change, which will be key to successfully implementing the roadmap and domestic cross-border payment priorities.

Focus area progress

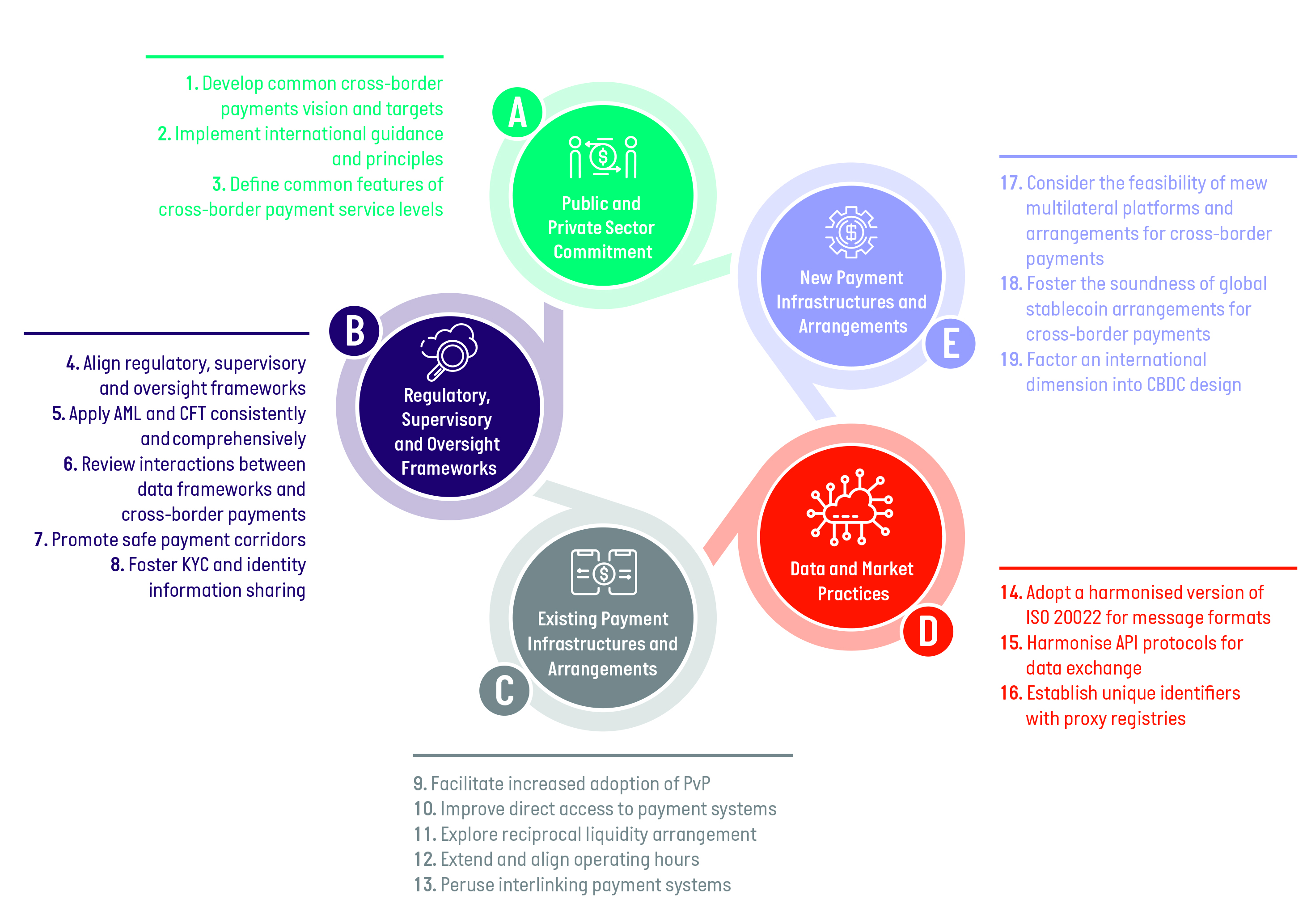

Focus Area A: Public and Private Sector Commitment

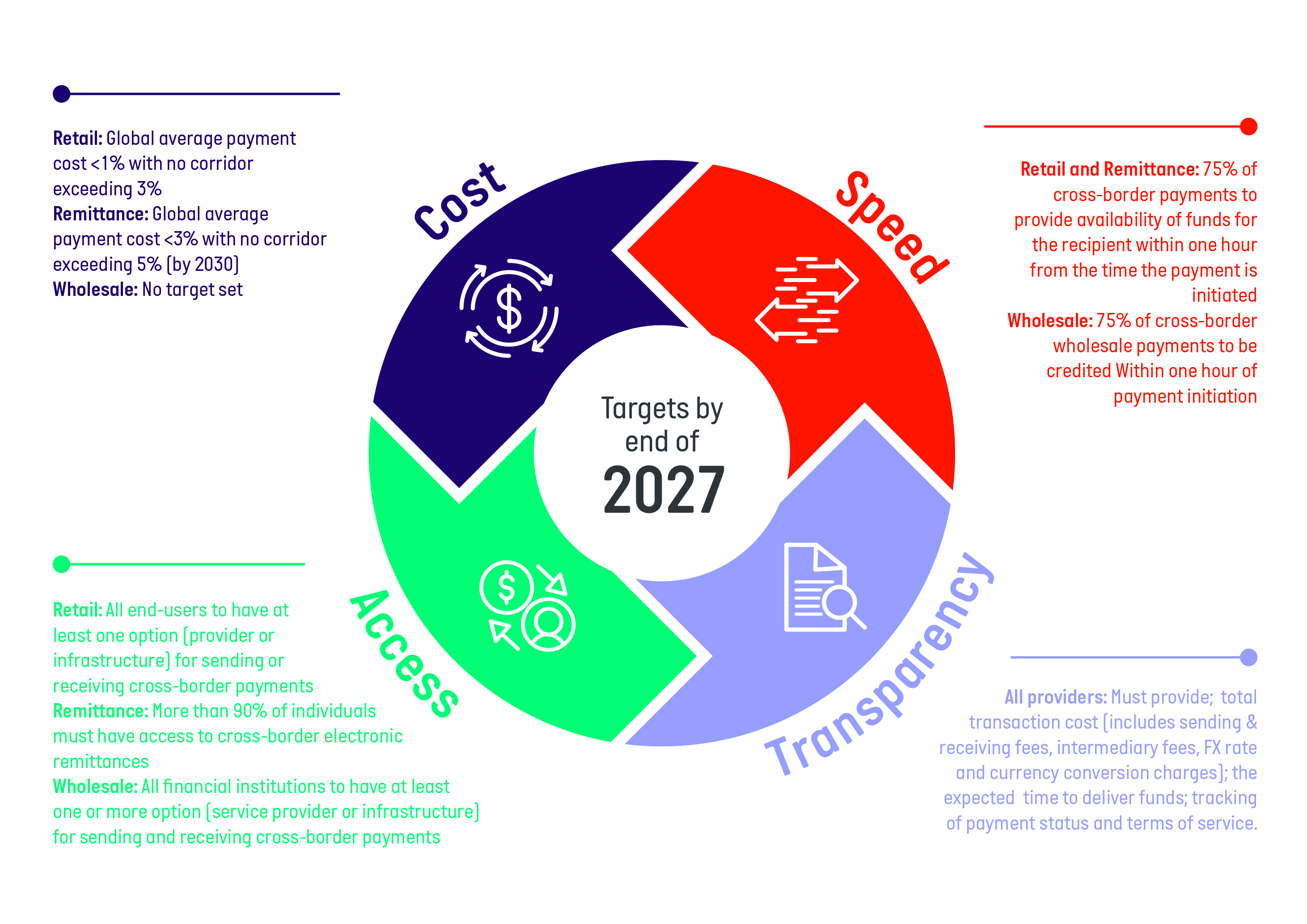

In October 2021, the FSB published its final report on ’Targets for addressing the four challenges of cross-border payments’, which included input from a consultation to which AusPayNet responded in July 2021.

In July 2022, the FSB outlined its preferred data collection and publication methodology in its interim report, ‘Developing the Implementation Approach for the Cross-Border Payments Targets’. AusPayNet responded to the feedback questions on the data collection methodology.

AusPayNet is currently working with our members on benchmarking Australia’s performance against the challenge of speed. See Appendix 1 for the key performance indicators.

Focus Area B: Regulatory, Supervisory and Oversight Frameworks

In December 2021, the International Monetary Fund (IMF) and World Bank published ‘A draft framework for money laundering/terrorist financing risk assessment of a remittance corridor’. The objective of this framework is to guide national regulators and law enforcement in collaborating to perform corridor risk assessments, which underpin the identification of safe remittance corridors (SRC).

In an Australian context, the Australian Transaction Reports and Analysis Centre (AUSTRAC) undertook some initial work on remittance corridors in 2017, which was funded by the Commonwealth Department of Foreign Affairs and Trade (DFAT).

Focus Area C: Existing Payment Infrastructures and Arrangements

In December 2021, CPMI issued its consultative report on ‘Extending and aligning payment system operating hours for cross-border payments’. AusPayNet engaged with its high value clearing system (HVCS) members and submitted the final response to CPMI in January, 2022.

In May, CPMI published their final report on ‘Extending and aligning operating hours of key payment systems’. In Australia, the New Payments Platform could be used for one or more interbank legs of a cross-border payment, based on correspondent banking arrangements. CPMI cited this particular approach in its final report as a means to enhance the speed of 24/7 cross-border payments.

The Report for National Authorities with respect to Building Block 10 (Improving access to payment systems for cross-border payments: best practices for self-assessments) was also published in May 2022. The paper provided detailed guidance in three key areas:

- the benefits, risks and barriers that central banks and payment system operators need to consider when assessing the case for expanding access to payment systems

- a detailed framework that can be used by central banks and payment system operators that are considering expanding access for self-assessing the access policies of domestic payment systems based on best practices

- existing examples and lessons learned through case studies of jurisdictions that have successfully expanded access and overcome existing barriers.

The RBA received the report, and it has also been distributed to AusPayNet’s HVCS members.

In July, CPMI published their Report to the G20, ‘Interlinking payment systems and the role of application programming interfaces: a framework for cross-border payments’. This paper focuses on interlinking of cross-jurisdictional fast payment systems (for example, if the NPP was to interlink with the National Payments Corporation of India’s UPI system) and provides guidance for establishing interlinking, so that these arrangements are supported by appropriate standards and legal agreements.

Focus Area D: Data and Market Practices

In April 2022, AusPayNet was invited to attend a restricted outreach session with the FSB and other sector participants to discuss Building Block 16 (Unique identifiers and proxy register for cross-border payments). There was general agreement regarding participants potentially expanding Legal Entity Identifiers (LEI) to a broad range of legal entities. There was also a great deal of discussion regarding the use of identifiers for natural persons. Specifically, it was recommended that the FSB perform a deep dive on the use cases, bearing in mind the particular complexities of cross-jurisdictional privacy frameworks. The FSB is continuing with its deep dive into use cases.

In July, the FSB published ‘Options to improve adoption of the LEI, in particular for use in cross-border payments’ (Building Block 16). This paper recommends broader use of the LEI globally, including within cross-border payments.

In Australia, LEI usage is governed by the Australian Securities and Investments Commission (ASIC) and is required for derivative transaction reporting (Regulatory Guide 251). Usage outside of derivative transaction reporting, particularly in cross-border payments, is limited. The Payments Market Practice Group (PMPG), in its white paper ‘Global adoption of the LEI in ISO 20022 Payment Messages - 2021' notes that there a number of jurisdictions that either mandate or are considering mandating the use of LEIs. The PMPG white paper also provides market practice for LEI usage within ISO 20022 payment messages. While LEI usage is not mandated in Australia for payments, it is, for example, an optional element within the new HVCS ISO 20022 messages.

Focus Area E: New Payments Infrastructures and Arrangements

In July 2022, the BIS Innovation Hub, CPMI, IMF and the World Bank published a report to the G20, ‘Options for access to and interoperability of CBDCs for cross-border payments’ (Building Block 19).

In November 2021, AusPayNet responded to a joint consultation by CPMI and Board of the International Organization of Securities Commission (IOSCO) on the ‘Application of the principles for financial market infrastructures to stablecoin arrangements’ (Building Block 18). In July 2022, CPMI and IOSCO published their guidance on the application of these principles, which was distributed to the members of the former working group of the Australian Payments Council who contributed to AusPayNet’s response. CPMI and IOSCO believe that the guidance is useful for stablecoin arrangements, including the relevant authorities charged with implementing these arrangements.

The FSB’s roadmap progress

In his April 2022 letter to the G20 Finance Ministers and Central Bank Governors meeting, held in Washington DC, the FSB chair noted the profound change to the global economy and financial markets caused by events such as the Covid 19 pandemic and Russia’s invasion of Ukraine. Despite this change, the FSB is continuing to coordinate work to advance the G20 cross-border payments roadmap. The FSB will further update the G20 Leaders on its progress at November’s G20 Leaders' Summit in Bali, Indonesia.

The G20’s commitment

The G20 Leaders are due to meet in Bali, Indonesia in November 2022. We anticipate that they will once again re-affirm their commitment to the G20 cross-border payments roadmap.

The G20 Finance Ministers and Central Bank Governors have re-affirmed their commitment in their communique.

What's planned for the rest of 2022

CPMI has commenced consultations on facilitating increased adoption of payment versus payment (PvP). AusPayNet is coordinating a response from its members.

We are expecting additional reports and guidance on stablecoin arrangements and Central Bank Digital Currencies. We are also expecting additional reports on digital identities and liquidity bridges.

As consultations and artefacts are produced, AusPayNet, through the CBPAC, will coordinate responses and activities to ensure the Australian payments industry is represented and prepared.

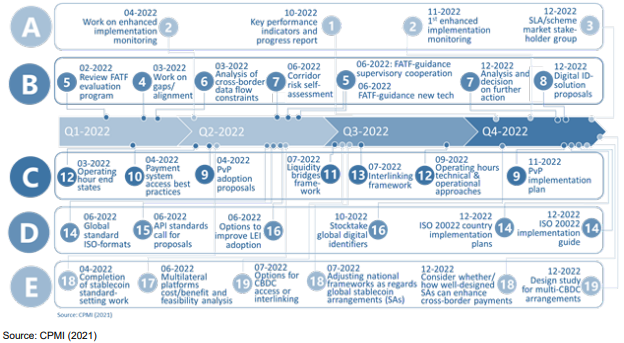

Taking forward the roadmap - CPMI milestones committed for 2022

AusPayNet Summit 2022: Paving the Way

Registrations are now open for the 2022 AusPayNet Summit, which will be held at the International Convention Centre (ICC) Sydney on Wednesday, 14 December and hosted by award-winning journalist and presenter, Helen Dalley.

This years Summit, themed ‘Paving the Way’ will feature a who’s who in payments in a dynamic series of interviews, panel discussions and rapid-fire talks. These will include an address by RBA Governor Philip Lowe; and Australia’s Assistant Treasurer and Minister for Financial Services, The Hon Stephen Jones MP, who will outline the role of government in payments; as well as the ‘Big Debate’, on Australia’s readiness for digital currency.

This event also provides a great opportunity for banking and payments industry professionals to network and make new connections.

More details about the Summit program and registrations can be found here.

We look forward to working with you through 2023.

Contact:

David O’Mahony

E: domahony@auspaynet.com.au

Please reach out if you would like further information or if there are any particular topics that you would like us to cover in future newsletters.

Appendix 1

| Wholesale | Retail (e.g. B2B, P2B/B2P, Other P2P3) | Remittances | |

|---|---|---|---|

| Cost | No Target Set | Global average cost of payment to be no more than 1%, with no corridors with costs higher than 3% by end-2027 | Reaffirm UN SDG: Global average cost of sending $200 remittance to be no more than 3% by 2030, with no corridors with costs higher than 5% |

| Speed | 75% of cross-border wholesale payments to be credited within one hour of payment initiation or within one hour of the pre-agreed settlement date and time for forward dated transactions and for the remainder of the market to be within one business day of payment initiation, by end-2027. Payments to be reconciled by end of the day on which they are credited, by end-2027. | 75% of cross-border retail payments to provide availability of funds for the recipient within one hour from the time the payment is initiated and for the remainder of the market to be within one business day of payment initiation, by end-2027 | 75% of cross-border remittance payments in every corridor to provide availability of funds for the recipient within one hour of payment initiation and for the remainder of the market to be within one business day, by end-2027 |

| Access | All financial institutions (including financial sector remittance service providers) operating in all payment corridors to have at least one option and, where appropriate, multiple options (i.e. multiple infrastructures or providers available) for sending and receiving cross-border wholesale payments by end-2027 | All end-users (individuals, businesses (including MSMEs) or banks) to have at least one options (i.e. at least one infrastructure or provider available) for sending or receiving cross-border electronic payments by end-2027 | More than 90% of individuals (including those without bank accounts) who wish to send or receive a remittance payment to have access to a means of cross-border electronic remittance payment by end-2027 |

| Transparency | All payment service providers to provide at a minimum the following list of information concerning cross-border payments to payers and payees by end-2027: total transaction cost (showing all relevant charges, including sending and receiving fees including those of any intermediaries, FX rate and currency conversion charges); the expected time to deliver funds; tracking of payment status; and terms of service. | ||