CEO's Corner

The final quarter of 2017 culminated in the establishment of two exciting new forums for industry collaboration: the Australian Payment Summit and the P7 Think Tank.

The final quarter of 2017 was consistent with the whole of the calendar year, passing at lightning speed, culminating in the establishment of two exciting new forums for industry collaboration. The first of these is in the form of a new global payments think-tank, and the second is a new Australian payments summit.

We are grateful to have initiated and hosted the P7 Think Tank, a new APAC and pacific rim collaboration involving seven prominent payment organisations. This group will meet annually to exchange insights and perspectives on payment trends, innovation, challenges and emerging strategic themes.

One of the standout lessons from our first P7 Think Tank is that the East has spearheaded an app-based approach to payments innovation. And this type of innovation has spread beyond China and India to many other Asian countries. This has resulted in an explosion of payment apps that support the introduction of further technology - such as audio QR, that enable rapid and frictionless transfer of value via mobile phones. These new Asian developments are not limited to app-based solutions but also include innovative initiatives such as the recent collaboration in the form of an MOU between five Asian countries to address real-time cross-border payments.

These developments in Asia underpin a theory recently put forward by the World Economic Forum (WEF) about nascent regionalisation of payment centres. The WEF argues that three regional payments centres are developing, each with its own unique technology and infrastructure characteristics. The first, emanating from the East and led by China, is the world of app-based payments centred on the mobile phone. In this paradigm, traditional point-of-sale and card-based payments are fast becoming obsolete. The second centre, based in Europe, is dominated by a new world where open data supports the entrance of new participants, leading to the introduction of unique new payments solutions. The third and final regional centre is in the US, where the world of card and point-of-sale remain central to the payments economy.

If the WEF is correct, and I would argue their perspective has merit, then the question to ponder is where will Australia land in our five to ten year horizon. I see an argument emerging that aligns our economy to Europe, as we move towards a world of open data. However, the Asian mobile app-centric model also seems plausible.

Australia's payment economy is sophisticated. On the one hand, we have world-leading tap and go payment behaviour, with contactless payments now accounting for 66% of in-store purchases. On the other hand, we have exceptionally high levels of smartphone penetration, and according to PayPal's 2017 mobile commerce index, 65% of Australians have shopped via a mobile app.

I look forward to the year ahead during which we will be involved in helping our own future take shape and unfold. Perhaps we will create a fourth payment centre of our own!

On a final note, I'd like to thank all our members and stakeholders for the invaluable contributions that made our inaugural Australian Payment Summit a day to remember. We will be in touch to learn how we can grow this event in 2018.

AusPayNet Events

We were delighted at the attendance and enthusiastic support for our inaugural Australian Payment Summit.

Australian Payment Summit

Our inaugural Australian Payment Summit held in December brought together over 250 participants to discuss key trends in payments in Australia and around the world.

We were delighted to have Dr Philip Lowe, Governor of the Reserve Bank of Australia, present the opening keynote. In examining a series of working hypotheses around whether the RBA intends to issue an eAUD, Dr Lowe shared insight into the RBA's perspective on what the future might look like.

The theme for the summit: "Towards a New World of Payments", included deep-dive discussions around digital identity, open banking and payments fraud, often drawing on UK and European experiences.

For more details about the event click the link below to our recent blog post. To remain up-to-date with details of our 2018 events, please get in touch.

Australian Payment Summit BlogSelected Articles See All >

Industry News

There have been a number of changes to the AusPayNet Board.

We publish payments fraud data twice-yearly. The December 2017 release, covering the 12 months to 30 June 2017, reflects recent trends.

Board Updates

In recent months, there have been a number of changes to our Board.

Paul Franklin, General Manager Payments at National Australia Bank joined the AusPayNet Board in October 2017, replacing Rosanna Fornarino.

Mr Franklin has also taken over as Chairman of the cheques clearing system (APCS) management committee, a role held by Ms Fornarino since joining the Board in February 2016.

Olivia McArdle, Head of Deposits and Payment Products at Macquarie Bank Limited, was elected to the Board by Electing Members in November 2017.

Ms McArdle fills the vacancy left by Simon Babbage's resignation earlier that month, after serving on the Board since October 2016. Ms McArdle also replaces Mr Babbage as Chairman of the high value clearing system (HVCS) management committee, and serves as member of the Remuneration and the Audit, Risk & Finance committees.

We extend a warm welcome to Mr Franklin and Ms McArdle, and thank Ms Fornarino and Mr Babbage for their contribution.

Director role rotation

We are pleased to advise that Anne Collard has been appointed AusPayNet Deputy Chair and Michelle McPhee, Chair of the Audit Risk and Finance Committee.

They replace Stuart Woodward and David Jay, who stepped down from the respective roles after completing two consecutive terms in December 2017. We extend our appreciation to Mr Woodward and Mr Jay. Both directors helped to significantly shape the Company during their terms in these roles. Mr Woodward continues to serve as Chairman of the Fraud in Banking Forum and Mr Jay as a member of the Nomination Committee.

Click here for more details on the AusPayNet Board.

Payment Card Fraud

The interim payments fraud data we released in December 2017 reflect recent trends. Chip technology is providing strong protection against counterfeit cards, and most card fraud is occurring in the online space.

Australians made more than $730.1 billion worth of card transactions in the 12 months to 30 June 2017 - a 3.8% increase on the previous year. Card fraud increased at a slightly lower rate - 3.1% - to $538.2 million. Within this fraud total:

- Counterfeit/skimming fraud dropped 34% to $42.2 million.

- Card-not-present (CNP) fraud increased 10% to $442.9 million now accounting for 82% of all fraud on Australian cards.

The significant drop in counterfeit/skimming fraud is likely due to the industry's roll-out of chip-reading at ATMs in Australia and close cooperation with law enforcement, as well as the steady adoption of chip technology in the United States. As a result, fraud is migrating to online channels. Other factors to consider are the popularity of online shopping and the global trend in cybercrime.

Tackling CNP fraud remains a high priority for industry. Next month, we are holding a stakeholder Accelerator Forum, in co-operation with the Reserve Bank of Australia, to expedite industry-wide solutions for addressing CNP fraud in Australia. Please get in touch if you would like more information.

A comprehensive payments fraud report covering data from 1 Jan to 31 Dec 2017 is due for release in mid-2018.

Fraud StatisticsRegulatory Round-up

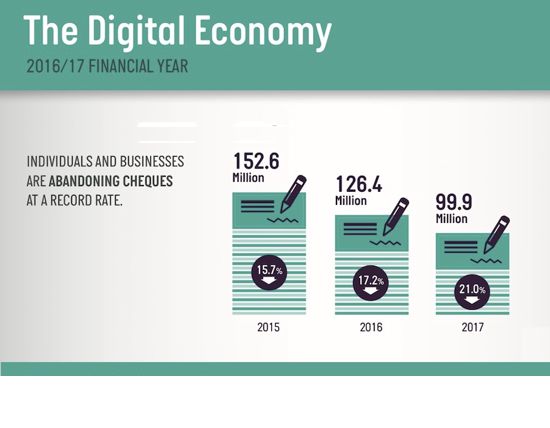

This quarter, we responded to the Government's consultations on the Digital Economy, and the Review into Open Banking in Australia.

The Digital Economy: Opening up the Conversation

In late 2017, we responded to the Government's consultation paper, The Digital Economy: Opening up the Conversation.

The consultation had a broad scope including areas relevant to the payments industry such as digital technology and infrastructure, data sharing, standards, cybersecurity and digital literacy.

Among other things, our submission highlighted that:

- Australia's world-class payments system underpins our digital economy. In recent years, the industry has invested heavily to build new infrastructure, to ensure it continues to support Australia's digital economy into the future.

- The digitalisation of the global economy presents both challenges and opportunities to the payments system. A self-regulatory approach, which has helped deliver Australia's world-class payments system, continues to be the most appropriate way to navigate these challenges.

- With the emergence of new business models, government also has an important role to play in ensuring the safe and efficient adoption of new technology through the creation of principles and guidelines in addition to public infrastructure investment and fostering digital literacy for all Australians.

The Government will use the review to inform its Digital Economy Strategy, which will focus on how Australia can adjust to seize the benefits of digital transformation. Minister Sinodinos noted that the performance of Australia's digital economy has been mixed. Analysis by McKinsey suggests digital technologies could contribute between $140-$250 billion to Australia's GDP by 2025. The Digital Economy Strategy would be "a forward-looking plan to maximise the potential of digital technology to improve the nation's productivity and competitiveness, while minimising its negative effects".

The Government is expected to launch its Digital Economy Strategy in the first half of 2018.

Our submission to the Digital Economy Conversation can be accessed by clicking on the link below.

Review into Open Banking in Australia

With open banking now launched in the United Kingdom, industry and government in Australia continue to explore the implications and requirements for our jurisdiction.

In late 2017, we responded to a Government Issues Paper, Review into Open Banking in Australia. The Paper canvassed views on the most appropriate model for Open Banking in Australia, a regulatory framework under which an Open Banking regime should operate, and a roadmap and timetable for its implementation.

Our submission highlighted that an open banking regime should be underpinned by a robust governance framework. This will help ensure that all parties, including consumers, data providers and third parties have confidence in the system. At a minimum, an effective governance model must be transparent, open to all participants (provided they are licensed and accredited), facilitate new technologies and consumer needs, and champion consumer interests.

The payments industry is of the view that participants should come together to agree a governance structure and operating rules, and that there must be continuous management through an accreditation regime.

The report of the Open Banking review was due to the Treasurer, Scott Morrison by the end of 2017. The Government is understood to be considering the report and looking to release a response in early 2018.

Our submission to the Open Banking Review can be accessed below.

Update on Productivity Commission Reviews: Data Availability and Use and Competition in the Australian Financial System

In July 2017, the Productivity Commission (PC) commenced an inquiry into Competition in the Australian Financial System.

The Consultation Paper released at that time identified the payments system as foundational infrastructure for our financial system. A Draft Report is slated for release shortly after Australia Day, with the Final Report due in July 2018.

While the Government has yet to formally release its full response to an earlier report from the PC into Data Availability and Use, it has announced the adoption of one of the Report's core recommendations. On 26 November 2017, Angus Taylor, Minister for Digital Transformation, announced that the Government will bring forward legislation for a national Consumer Data Right in 2018. The Consumer Data Right will allow customers open access to their banking, energy, phone and internet transactions.

Both inquiries were established as a result of recommendations made in the 2014 Financial Systems Inquiry: to periodically review the state of competition in the sector, and to review the costs and benefits of increasing access to and improving the use of data.

Submission - The Digital Economy Submission - Open Banking Review