In this Issue

-

CEO’s Corner

-

- Modernising Australia’s Payments System

-

- Consultation on Reforms to the Payment Systems (Regulation) Act 1998 (PSRA)

-

- Consultation on Licensing of Payment Service Providers (PSPs) – payment functions

-

- A Strategic Plan for Australia’s Payments System

-

Update on payments reforms

-

- Responses to the Consultations on Payment System Reforms

-

- Response to the Consultation on Modernising Australia’s AML/CTF Regime

-

- Response to the Consultation on Safe and Responsible AI in Australia

-

Economic Crime Forum (ECF) update

-

- Australian Payment Fraud Report

-

AusPayNet’s program to become an authorised standards-setting body (ASSB)

-

ISO 20022 migration

-

Advanced Encryption Standard (AES) migration program update

-

Update on legacy payment systems

-

- Cheques

-

- BECS

-

Cross-border payments update

-

Blog posts

-

AusPayNet Summit 2023

-

Stakeholder engagement update

CEO’s Corner

Modernising Australia’s Payments System

It is now two months since the Government made its announcement on modernising Australia’s payment system. It is therefore timely to review progress since our initial response. We do so by looking at the two consultations launched as part of that announcement, before concluding with some comments on three elements of Government’s Strategic Plan for Australia’s Payments System.

Consultation on Reforms to the Payment Systems (Regulation) Act 1998 (PSRA)

The consultation proposes broadening the PSRA’s definitions of ‘payment system’ and ‘participant’. This is sensible to ensure that they capture all entities involved in the payments value chain. Developments in the Australian payments ecosystem over the past decade mean that the existing definitions no longer do so. This can create an uneven playing field between different providers of payment services, and undermine the RBA’s ability to respond to these developments.

The consultation’s stated intention to retain the PSRA’s presumption in favour of self-regulation – for example, in the comment that, “being within scope of regulation does not mean a participant will be regulated … such a decision [to regulate] would typically only be made after considering whether non-regulatory solutions could address the relevant concerns” – is also sensible; it continues to serve Australia well.

One idea AusPayNet raised in our submission to the consultation was whether, since the PSRA is the legislative foundation for the RBA’s powers on payments, Treasury could establish the RBA’s new powers to both develop common access requirements, and authorise and oversee industry standard-setting bodies as part of this review of the PSRA. Suitable caveats would be needed to link the exercise of these powers to the establishment of the PSP licensing framework. However, granting these powers now could enable some of the proposed rights and obligations associated with that framework to take effect as soon as it is established, rather than requiring an additional round of legislative amendments.

Consultation on Licensing of Payment Service Providers (PSPs) – payment functions

Similar to the point made above on the need for comprehensive definitions of ‘payment system’ and ‘participant’, a tailored licensing regime for all PSPs will help promote access and competition while appropriately controlling risk. Defining the payment functions that should be captured – the focus of this consultation – is a critical first step in establishing the foundations for this licensing framework.

International experience shows that there are several ways of classifying the many different activities undertaken by PSPs. However, the proposed list of payment functions outlined in the consultation, including the high-level differentiation between stored-value facilities (SVFs) and payment facilitation services (PFSs) is a good approach, akin to best practice elsewhere (e.g. in Europe).

In our submission, however, we suggest some amendments to the approach, as follows:

- Greater clarity for entities that are likely to fit into more than one functional category, such as payment system operators

- That the storage of payment and transaction data and the provision of security services do not appear to – but should – be captured within the proposed list of payment functions

- That while the consultation paper seeks feedback on whether PFSs that are not consumer-facing should be required to hold a licence, AusPayNet’s view is that all PSPs should be licensed, regardless of whether there is a direct consumer relationship or not.

One of the stated objectives of the new licensing regime is to better align regulatory obligations to the level of risk posed by a PSP. AusPayNet’s preliminary view is that some level of tiering or gradation (of licences and/or obligations) is likely to be required to achieve the objective of balancing end-user and financial system protection with regulatory burden, and better aligning with the principle of ‘same risk, same rules’ regulation.

The consultation also provides a useful high-level categorisation of the key risks associated with different payment functions. We suggested considering additional factors that may affect a PSP’s risk profile, such as scale, nature of business, customer base, transaction values and volumes, and enabling technology. We also suggested considering whether more detailed risk management requirements should apply to all PFSs, particularly around operational risk, as is the case in Canada, Singapore and the UK.

A Strategic Plan for Australia’s Payments System

In his presentation of the Strategic Plan, the Treasurer noted that “leaving cheques in the system is an increasingly costly way of servicing a declining fraction of payments”. He also noted that the “transition will be gradual, coordinated and inclusive”. This will start with a government consultation on the topic later in the year.

Another priority outlined in the Strategic Plan was action on scams. Pleasingly, there has been real progress here, with the National Anti-Scam Centre (NASC) having launched on 1 July and immediately announced its first fusion cell, targeting investment scams. I am representing AusPayNet on the NASC’s Advisory Board.

Finally, on cybersecurity, the Plan noted the need for an “uplift in system-wide security standards and practices relating to the security standards and encryption methods for card payment systems” and that, given this, “AusPayNet has commenced planning for an industry-wide program to migrate the Australian card payments system to the safer Advanced Encryption Standard”. This program is now in its mobilisation phase, which will continue until December 2024. This phase includes the preparatory activities to finalise the technical blueprint, testing strategy, and migration approach.

Update on payments reforms

AusPayNet continues to engage with Government stakeholders, regulators and departments on the following consultations:

Responses to the Consultations on Payment System Reforms

As outlined in CEO’s Corner, AusPayNet submitted responses to two consultation papers underpinning part of the Government’s payment system reform agenda: Reforms to the Payment Systems (Regulation) Act 1998 (PSRA) and Payments System Modernisation (Licensing: Defining Payment Functions).

We look forward to continuing our engagement with Treasury and Members on the payment system reforms, including through the upcoming consultation on the regulatory obligations that would apply under the new PSP licensing framework.

Response to the Consultation on Modernising Australia’s AML/CTF Regime

In June, AusPayNet responded to the Attorney-General’s Department’s consultation on modernising Australia’s anti-money laundering and counter-terrorism financing (AML/CTF) regime. The AML/CTF regime is a critical part of Australia’s efforts to prevent criminals from receiving the proceeds of their illegal activity and stopping funds from falling into the hands of terrorist organisations. As observed in the consultation paper, the regime has not kept pace with the changing threat environment and evolving international standards, resulting in gaps and vulnerabilities that could have significant economic and social consequences for Australia.

In line with AusPayNet’s commitment to working with Members, government and other stakeholders to defend the payments system from economic crime, our submission welcomed the review of the AML/CTF regime to ensure that it remains clear, fit-for-purpose and meets international standards and best practice. We expressed support for:

- Simplifying and modernising the AML/CTF regime to help businesses better understand and comply with their obligations, and promote consistency in application across entities

- Amending the tipping-off offence to enable greater collaboration between financial crime teams across the ecosystem, to facilitate the detection and disruption of economic crime

- Expanding the AML/CTF obligations to digital currency exchanges and tranche-two entities, in line with the international Financial Action Task Force (FATF) Standards

- Updating and simplifying the customer due diligence obligations, including to reflect developments in identification technology and processes

- Ensuring that any changes to the travel rule obligations account for the data limitations of Australia’s direct entry system, to ensure that BECS can continue to support the settlement of the significant share of Australia’s payment transactions that it does currently.

Response to the Consultation on Safe and Responsible AI in Australia

In August, AusPayNet responded to Government’s consultation on supporting responsible artificial intelligence (AI) in Australia. AI has the potential to deliver significant benefits across all areas of Australia’s economy and society. The payments ecosystem has been using AI technology for several years to drive innovation, efficiency and safety for businesses and consumers. However, the ongoing developments in AI also have the potential to generate significant risks if not designed and deployed responsibly. This can deter adoption and limit Australia’s opportunity to capture the full benefits of this technology.

AusPayNet supports the Government’s work to ensure that Australia has clear and proportionate governance frameworks in place to mitigate potential risks while supporting the continued development and adoption of effective and trustworthy AI technology.

Based on our review of global approaches to AI regulation and our experience in developing and managing standards for the payments industry, we propose adopting a sector-based approach in which regulators would seek to proportionately address the risks posed by AI within their respective remits, in accordance with existing laws and regulations and guided by a set of cross-sectoral principles on responsible AI. This would give regulators the flexibility to tailor their response to the use and impact of AI for specific contexts within their areas of expertise, while ensuring general consistency in outcomes across the economy.

Given the cross-border nature of technology, global coordination on governance will also be important for facilitating the development and adoption of AI technologies. We also encourage the Government to consider measures that would assist businesses in adopting AI technology, including the provision of tools to help verify that an AI-enabled system meets the necessary standards.

Economic Crime Forum (ECF) update

As we have noted before, we stand at a generational tipping point in payments, with two once-in-a-lifetime opportunities:

- to modernise payments regulation

- to simplify the payments system.

However, alongside these generational opportunities, we have one generational obligation: to mitigate scams, which unfortunately affect far too many Australian consumers and businesses.

AusPayNet is a member of the National Anti-Scam Centre (NASC) Advisory Board and the NASC’s investment scam fusion cell. To support the NASC and ACCC, we continue to leverage our Economic Crime Forum (ECF).

In August, the ECF met in Canberra and discussed appropriate friction in payments and initiatives to disrupt money mule accounts, and continued to develop intelligence packages for law enforcement to disrupt transnational organised crime engaging in scams.

AusPayNet remains ready to contribute to the forthcoming consultation on national anti-scam codes.

Australian Payment Fraud Report

AusPayNet’s 2023 Australian Payment Fraud Report highlights that in 2022, the fraud rate was 57.5 cents per $1,000 spent, up slightly from 57.3 cents in 2021. Card fraud increased by 16.5% from the previous year, to $577 million, in line with the increase in total spending on cards, which rose 16% to $1 trillion over the same period.

The data indicates that the fraud rate has stabilised since the introduction of the industry’s card-not-present (CNP) Fraud Mitigation Framework in 2019, with the 2022 fraud rate remaining well below the fraud rate of 75.0 cents per $1,000 spent in 2017.

CNP fraud accounted for 90% of all fraud on Australian cards in 2022, increasing by 14.4% from 2021 to $516.8 million, reflecting the sustained and rapid rise in e-commerce, which accelerated during the COVID-19 pandemic.

CNP fraud actually declined in Australia (by 4.8%), but CNP fraud overseas (on Australian-issued cards) increased almost 50%. The CNP Fraud Mitigation Framework only applies to merchants based in Australia.

Cheque fraud dropped 24% to $2.4 million in 2022, in line with the rapid consumer decline of cheques as a method of payment.

For more figures and insights, read the 2023 Australian Payment Fraud Report on AusPayNet’s website.

AusPayNet’s program to become an authorised standards-setting body (ASSB)

AusPayNet continues its work developing a framework for becoming an ASSB for the payments industry. We have designed, and are currently consulting on, a proposed governance model, funding principles and high-level model for standards development and enforcement.

The following broadly details the proposed model:

- A panel will make decisions relating to approval and enforcement of standards.

- The panel will be made up of independent experts, appointed by a panel appointment committee.

- The panel will have the power to make its own decisions, subject to two caveats: firstly, it will be expected to consult with relevant regulators in relation to the approval of standards (to ensure those standards meet regulatory requirements). Secondly, it will be required to inform ASIC of issues that may need to be investigated as a potential breach of the Corporations Act.

- The panel’s work will be subject to an external assurance review mechanism to ensure it meets its objectives.

- AusPayNet’s Board will appoint the panel appointment committee and will have ultimate responsibility for ensuring the standards-setting body (as a whole) retains its authorisation and performs in accordance with requirements set by the RBA.

- The ASSB work will be funded by licensees on a fixed and tiered fee basis.

AusPayNet continues to design the operating models for the various components of the ASSB function and is developing a detailed pipeline of technical standards that are likely to be in scope for the ASSB. AusPayNet will formally consult with the industry, regulators, and other key stakeholders on both of these pieces of work in due course.

ISO 20022 migration

For a high-level update regarding the progress of the ISO 20022 Industry Migration Program, please refer to the latest quarterly issue of Migration Monitor on AusPayNet’s website, published in July.

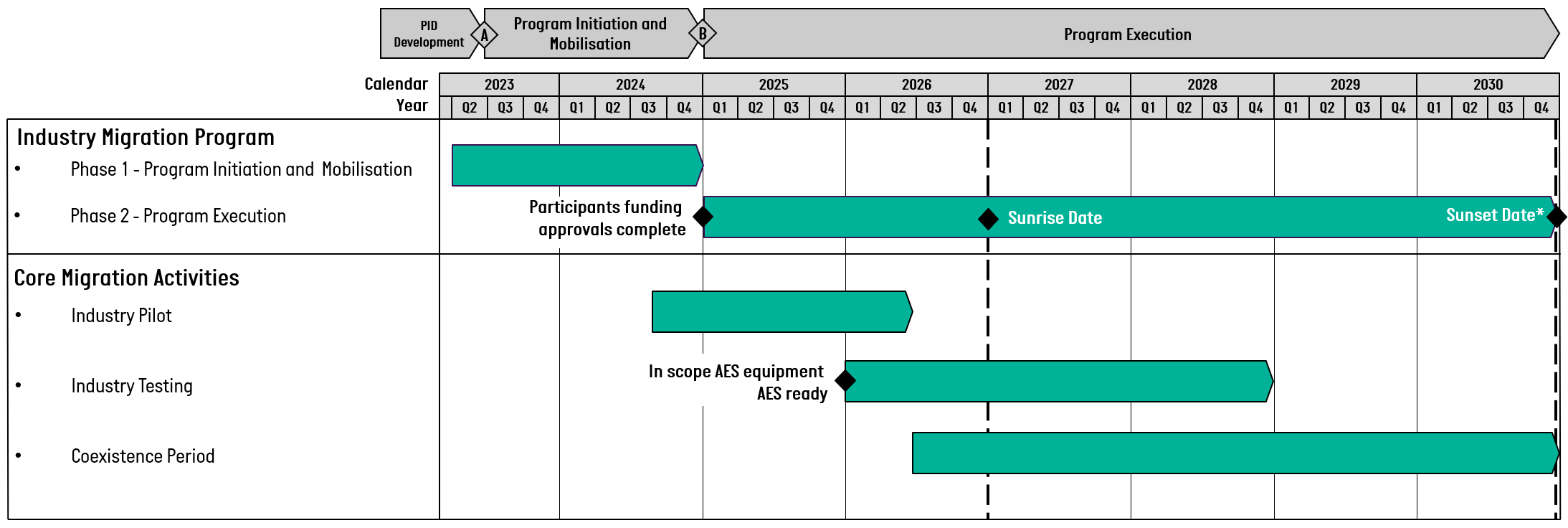

Advanced Encryption Standard (AES) migration program update

In December 2022, work commenced on developing a Program Initiation Document (PID) for the AES Migration Program, detailing the background, rationale, approach, and plan for migrating to AES for the national card payments system. A consultative approach was taken to developing the PID, allowing Members to review, endorse, and validate content for the PID through several working groups, representing Members from the Issuers and Acquirers Community (IAC).

Since December 2022, four iterations of working group meetings have been held, resulting in the final draft of the PID being endorsed in May 2023.

The plan to migrate to AES has two phases:

- Initiation and Mobilisation (July 2023 – December 2024): This phase includes preparatory activities to finalise outstanding issues – including the technical blueprint, testing strategy, migration approach, legal, risk and compliance assessment – to provide time for participants to formalise their business cases, secure funding, and mobilise teams. It is anticipated that participants will be ready to commence their programs by January 2025.

- Execution (January 2025 – December 2030): This phase includes industry readiness activities leading to an industry pilot, with migration to follow. An extended period of coexistence has been planned for the migration. This enables assets to be upgraded in line with their natural replacement cycles, as far as is possible, thus reducing marginal effort and cost. Execution will complete once all assets have been upgraded and TDES (Triple Data Encryption Standard) has been removed.

In July, work commenced on the first six months of the Initiation and Mobilisation phase, focused on the technical blueprint and options to approach the migration.

Update on legacy payment systems

In its Strategic Plan for Australia’s Payments System, Treasury says:

“A key priority for the Government is to ensure the payments system fosters the development of modern, efficient payment infrastructure that promotes greater financial inclusion and delivers a seamless user experience.”

According to the Plan, achieving this priority will include providing policy direction for legacy systems such as cheques and the Bulk Electronic Clearing System (BECS).

AusPayNet supports the policy outcomes described in the Plan and will continue to lead with its programs associated with the management of legacy payments systems.

Cheques

The Plan details a focus on phasing out government use of cheques by 2028 and, subject to consultation, expects the eventual wind down of the cheques system to happen no later than 2030.

AusPayNet continues to proactively respond to the customer-led decline of cheques with a program of work that commenced in 2019. This program has focused on ensuring that participants in the Australian Paper Clearing System Framework (Cheques Framework) can make their own individual choices, that we promote payment neutrality in legislation (both state and federal), and that we promote inclusivity through community and market education on the decline of cheque usage and availability of modern payment alternatives.

In line with the Plan, AusPayNet’s program will focus on:

- Community outreach: Liaising with industry groups, organisation and representative bodies that still use cheques to continue our education on the decline of cheques and modern payment alternatives.

- Government engagement: There remains a need to move to payment neutrality in legislation, not only to enable participants to adopt payment alternatives today, but also to future-proof that legislation for developments in payments technology. AusPayNet also looks forward to responding to Treasury’s consultation on the future of cheques, which is due to be released later this year.

- Operational efficiency: As usage continues to decline and participants of the Cheques Framework cease to use and offer cheques, it is important that operational processes are reviewed to help minimise any impact on users of cheques as well as operators of the cheques system.

BECS

BECS enables the processing of Direct Entry payments, including direct debits and direct credits, between individual accounts held at different Australian financial institutions. As the Plan observes, this system has served Australia well, enabling businesses, governments, and individuals to make both one-off and recurring payments since the mid-1990s. But since that time, more modern payment alternatives have emerged, that are equipped with greater functionality and capability.

AusPayNet has consulted with BECS members, users of the system and providers of payment alternatives to test the appetite for, and readiness to adopt, BECS alternatives. Consultation has confirmed that while a move away from BECS represents both opportunity and challenges, there is a strong case for change. Consultation also revealed that the readiness for adoption of alternatives varies depending on the specific BECS use cases. As an example, we have already seen the take up of payment alternatives for single payment use cases, whereas the preferred approach for processing bulk files continues to be BECS.

Following the consultation, AusPayNet is looking to set the strategic direction for the future of the BECS Framework. Over the coming months, target timeframes, industry monitoring and reporting, a governance structure, and a related communications plan will be developed. More detail on this plan will be available by the end of the year.

Cross-border payments update

Since delivering its Priorities for the next phase of work, the Financial Stability Board (FSB) has published its Priority actions for achieving the G20 targets. This articulates specific action items across the themes of:

- Payment system interoperability and extension

- Legal, regulatory and supervisory frameworks

- Cross-border data exchange and message standards.

In support of these themes, two taskforces have been established:

- The Committee on Payment and Market Infrastructures (CPMI) has established the Payment System Interoperability and Extension (PIE) Taskforce to bring together the public and private sectors to provide advice and coordination, and to plan implementation measures to improve market conventions and practices.

- The FSB has established the Legal, Regulatory and Supervisory (LRS) Taskforce, which brings together public and private sector experts to provide feedback and input on reducing the frictions from data, legal, regulatory or supervisory frameworks that impact cross-border payments.

In addition, an API Panel of Experts is being established to evaluate proposals for API standards in cross-border payment information exchange, to develop recommendations for greater harmonisation of APIs, and to develop a longer-term global governance proposal and process.

Australia has representation on both the PIE and LRS Taskforces and we look forward to working with our global peers to reduce the frictions experienced in cross-border payments.

These actions – identified by the FSB, CPMI and their partner organisations – in conjunction with the Taskforces, will be foundational in helping deliver the quantitative targets of faster, cheaper, accessible and transparent cross-border payments.

In April, we published the most recent issue of our Cross-Border Payments Round-Up, which provides a summary of the FSB’s activities, responses to consultations and other actions being undertaken to support and successfully implement the roadmap and domestic cross-border payment priorities. The next bi-yearly issue of the Cross-Border Payments Round-Up will be published in October.

Blog posts

AusPayNet regularly publishes blog posts, sharing important information and insights regarding Australia’s payments system. In case you missed them, our most recent posts are:

- Response to Government’s Announcement on Modernising Australia’s Payments System: Following the Government’s release of its Strategic Plan for Australia’s Payments System, AusPayNet CEO Andy White explained how the Plan will help to ensure the payments system is fit for the future, and highlighted work in which AusPayNet is already engaged that will contribute to realising the Government’s vision for payments

- The standards landscape in Australian payments: Paul Creswick, AusPayNet’s Security Evangelist, focused on the current and evolving standards landscape in Australian payments and the role of domestic standards. He also talked about the recent ISO 20022 migration and previewed future work around the AES migration.

AusPayNet Summit 2023

Following on from the sell-out success of our 2022 Summit, AusPayNet is excited to announce that tickets will go on sale this month for our 2023 event to be held at the International Convention Centre (ICC), Sydney on Tuesday, 12 December.

The theme of this year’s Summit is ‘A Turning Point’, resonant of the shift the industry has embarked on, including but not limited to, the presentation of the Government’s Strategic Plan for Payments and the appointment of Australia’s first female RBA Governor – both of which will play a critical role in shaping the future of payments in our country.

Be sure to take advantage of our early bird offer by Friday, 13 October and save $145 on individual and group registrations per person.

See our website or follow us on LinkedIn or X (formerly Twitter) for ticket and event updates.

Stakeholder engagement update

AusPayNet’s Stakeholder Advisory Council met earlier this month. As a reminder, this Council acts as an advisor to our Board as we seek feedback from non-Member stakeholders of the payments system on strategic and material matters.

At the recent meeting, we sought the Council’s feedback on the following items.

- Implications for AusPayNet of the Government’s Strategic Plan for Australia’s Payments System

- Treasury’s payments reforms consultations

- AusPayNet’s Corporate Strategy

- AusPayNet’s program to become an ASSB.

The Council’s feedback will be presented to AusPayNet’s Board shortly.

In July, we hosted the Government’s Treasury team for a Q&A session for our members to learn more about the Strategic Plan for Australia’s Payments System and the two consultations recently commenced by Government to ensure that regulations keep up with payments innovations. Over 270 individuals from Member organisations attended the virtual session, reflecting the importance of the Government’s proposed payments reforms. Members pre-submitted questions and our Chief Strategy Officer, Rajat Jain, hosted the session. We look forward to welcoming Members to more events in the coming months.

New members

AusPayNet is pleased to welcome:

- BioCatch (APAC) Pty Ltd as a PSP Member (effective 17 August)

- Optal Australia Pty Ltd as a PSP Member (effective 17 August).

For more information on AusPayNet membership, please visit our website.

Stay up to date!

Remember to follow AusPayNet on LinkedIn and X (formerly Twitter) to stay up to date with the latest news on the Australian payments system.

Additionally, make sure you subscribe to our mailing list to be alerted when blog posts and other new content becomes available.